CIPD-IRN Private sector pay and employment 2026

The annual CIPD–IRN private sector report captures changing pay and employment trends as well as the drivers of change in the labour market in Ireland

The annual CIPD–IRN private sector report captures changing pay and employment trends as well as the drivers of change in the labour market in Ireland

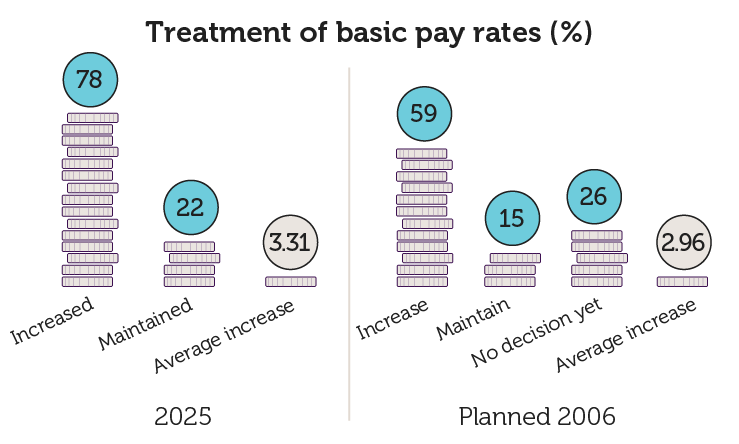

In 2025, 78% of private sector organisations increased basic pay (salaries), with an average pay rise of 3.31%. A smaller proportion (22%) maintained pay rates.

A clear downward trend in pay growth is emerging in the Irish private and semi state sector. Our survey shows average salary increases have been stepping down steadily over the past few years:

• 2022: 5.06%

• 2023: 4.38%

• 2024: 4.24%

• 2025: 3.31%

Implications: In previous CIPD/IRN surveys, we highlighted that planned pay increases are usually more conservative than actual, however last year it is fairly aligned. Planned for 2025 was 3.66% and actual was 3.31%. Alignment of planned and actual pay indicates disciplined financial planning and improved forecasting capability, reflecting the HR function’s growing role in linking remuneration strategy to business outcomes.

Looking ahead to 2026, average increases are projected to moderate to 2.96% overall, with the following trends:

Implications: This moderation, combined with easing inflation (1.7% Jan 2026), suggests organisations are exercising strategic cost discipline while adjusting reward strategies for sustained competitiveness. However, the outlook remains uncertain. Ongoing geopolitical tensions, with the potential to disrupt energy markets and global supply chains, could yet place renewed upward pressure on inflation echoing the supply-driven shocks experienced in 2022–2023. While it is too early to determine whether these risks will materialise, organisations may need to remain agile in managing pay expectations, particularly as labour market tightness and skills shortages continue to influence wage dynamics in some sectors.

Bonus strategies differ markedly by union status. Overall, 66% of organisations are planning bonuses in 2026. Non-unionised organisations are more likely to use bonus flexibility, with 34% offering bonuses to all employees, whereas 40% of unionised organisations report no bonus provision. This highlights the continuing reliance on base pay in collectively bargained environments.

Implications: HR leaders should recognise that bonuses are common in both unionised and non-unionised workplaces, and should be used strategically through collective agreements in unionised settings or discretionary schemes in non-unionised settings to reward performance and support retention.

Non-pay benefits are largely stable. While 25% of employers plan to increase benefits in 2026, 47% intend to maintain current provisions.

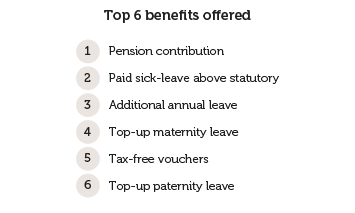

The top six benefits continue to include pension contributions with 91% of organisations marking this as a benefit, paid sick leave above statutory requirements, additional annual leave, top-up maternity and paternity leave, and tax-free vouchers. Tax-free vouchers are offered at varying levels, with the majority falling in the €251–1,000 range. Although interestingly, 23% of those giving tax-free vouchers were giving the maximum amount of €1,500.

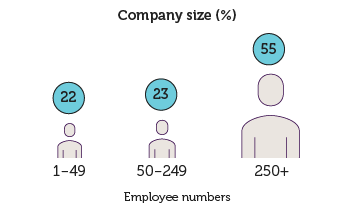

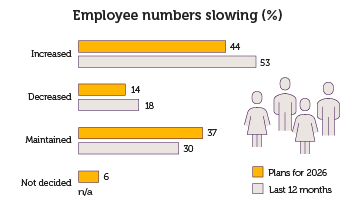

In 2025, 53% of organisations increased employee numbers, 18% decreased, and 30% maintained employee levels. Growth was strongest among mid-sized firms (150–249 employees) at 67%. Small firms (1–49 employees) saw only 38% increase headcount, with 50% maintaining numbers.

Planned changes for the next 12 months show a slowdown, with 44% intending to increase, 37% maintaining, and 13% planning to decrease. This trend indicates a cautious approach, particularly among larger employers, with the potential for small reductions in headcount reflecting broader market uncertainties.

Implications: These findings reinforce the need for scenario-based workforce planning and agile resourcing strategies.

Information and consultation forums remain underdeveloped, with only 39.6% of organisations having a forum in place. Just 15.6% are established under the Employees (Provision of Information and Consultation) Act 2006, and 24% are established outside the Act. Half of employers have no forum and are not planning one.

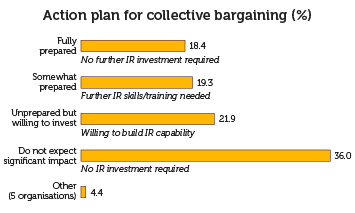

Readiness for collective bargaining appears mixed, with non-union collective bargaining declining from 11% in 2025 to 7% in 2026.

For the first time, organisations were asked about their readiness for collective bargaining in light of the Government’s Action Plan for the Promotion of Collective Bargaining, revealing a varied picture: 18% feel fully prepared, 19% are somewhat prepared but need additional skills, 22% are unprepared yet willing to invest in capability, 36% do not expect significant impact, and 4% fall into other categories.

Against the backdrop of Ireland’s Action Plan to Promote Collective Bargaining and EU legislation such as the Adequate Minimum Wages Directive, these findings highlight the importance of building industrial relations capability.

Implications: As EU directives on employee information and consultation, alongside upcoming pay transparency requirements, place greater emphasis on structured dialogue with employees, HR functions will need to ensure appropriate communication channels, consultation mechanisms and bargaining readiness are in place.

Insight from our HR practices in Ireland data suggest this may present a challenge for some organisations. While HR functions report relatively strong maturity in supporting employee experience, lower capability in areas such as people analytics and structured consultation indicates that some organisations may not yet have the infrastructure required to support emerging collective bargaining obligations.

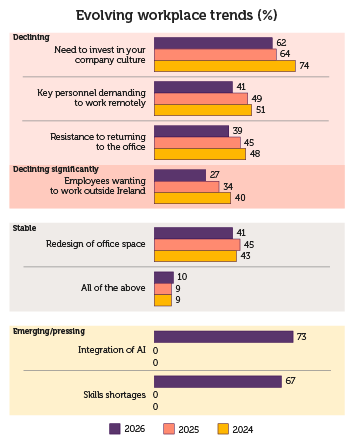

Trends from 2024 to 2026 highlight both persisting and emerging pressures. Investment in company culture remains high but is declining (62% in 2026, down from 74% in 2024), demand for remote work and resistance to returning to offices are declining trends, and employees wanting to work outside Ireland has fallen sharply from 40% in 2024 to 27% in 2026.

Conversely, emerging priorities include AI integration (73%) and addressing skills shortages (67%), indicating urgent focus areas for employers. Hybrid and remote working demand continues to affect 73% of employers, while pay and benefits, recruitment, wellbeing, retention, and diversity remain key operational concerns.

Implications: HR should prioritise technology upskilling, workforce reskilling, and flexible work arrangements to respond to evolving organisational needs. Insight from HR Practices in Ireland survey data shows full AI embedding remains below 6%, indicating a significant execution gap between strategic intent and operational capability. The AI adoption gap represents a critical capability risk, requiring investment in governance, process redesign, and digital literacy to realise the strategic benefits of automation.

Policy coverage continues to expand, particularly in areas linked to gender, health, and wellbeing. Menopause support has grown to 32%, fertility policies to 22%, miscarriage support to 36%, domestic abuse policies to 68%, menstrual health to 14%, and men’s health to 20%. These increases indicate a continuing commitment to progressive employee policies, particularly in larger and service-sector organisations.

Neurodiversity policies are emerging, with one-third of respondents reporting neuro-inclusion initiatives.

There were also indications from some respondents that additional support for parents could be beneficial, including initiatives such as “first day of school” leave and working parent coaching. While raised by a smaller number of respondents, these responses highlight emerging areas where HR could explore targeted family-friendly policies.

Implications: Expansion of progressive policies reflects operational necessity, particularly given that HR practices in Ireland research shows mental health accounts for 51% of absence causes, linking wellbeing directly to productivity and business continuity.

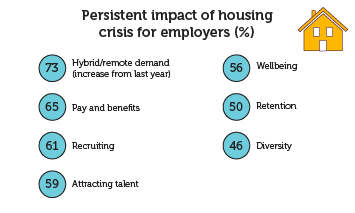

The housing crisis is increasingly constraining recruitment, with 61% of employers reporting housing shortages having a medium or high impact, rising to 71% among larger organisations. It has become a structural labour market issue, influencing recruitment, retention, pay, benefits, wellbeing, and diversity. Rising housing pressures are also driving demand for hybrid and remote work (73%), reinforced by the Code of Practice on the Right to Request Remote Work, now two years in effect.

Housing shortages represent a structural constraint on talent mobility and geographic deployment, directly impacting organisational competitiveness and workforce planning decisions.

Implications: The profession must implement flexible, supportive policies and consider location-based incentives or remote work options to attract and retain talent. HR Practices in Ireland survey data supports this, showing 80% of organisations report that hybrid work supports inclusion and 65% view it as the most productive model, flexible work has evolved from a preference to a strategic necessity in a housing-constrained labour market.

Ageing workforce strategies show mixed progress. While retirement planning support training remains high (56%), other initiatives such as age audits, age-friendly benefits, and training for older workers or managers show modest or declining adoption.

Organisations continue to explore strategies to support older workers, but uptake is inconsistent. This aligns with national trends: the number of people aged 65 and over in employment in Ireland increased by 26% between 2021 and 2025. OECD analysis highlights that sustaining employment at older ages depends on policies supporting continuous learning, flexible work arrangements, and healthy working lives, underscoring the need for more consistent adoption of ageing workforce strategies.

HR practices in Ireland data shows 61% of organisations identify line manager capability as their greatest constraint, the successful retention of older workers will depend heavily on targeted leadership and intergenerational management development.

Implication: Failure to embed structured ageing workforce strategies may create knowledge retention risks and increase replacement costs, highlighting the need for strategic succession planning and leadership capability development.

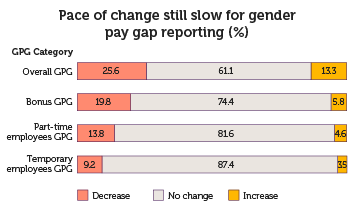

Gender pay gap (GPG) reporting shows limited impact in closing gaps, with 61% of employers reporting no change in their overall GPG, 25.6% reporting a decrease in their overall GPG, and 13.3% reporting increases.

Large employers are more likely to show EU Pay Transparency Directive progress through recruitment, progression, monitoring, and governance initiatives, while small firms demonstrate slower policy evolution. To assess preparedness for the new requirements, we asked whether organisations were publishing internal pay scales; only 28.5% reported doing so, with particularly low levels in small firms (4%) and manufacturing sectors (16%).

Implication: As joint pay assessments become a requirement under the Directive, organisations will need to go beyond reporting and actively evaluate pay practices across roles and categories of work. Planning and embedding a structured process for joint pay assessments now will help ensure compliance, identify inequities, and support fair pay governance. Pay transparency will increasingly become a governance requirement, requiring board-level oversight and robust HR data capabilities to mitigate regulatory and reputational risk.

Two-thirds of respondents prefer new hires to join existing pension schemes rather than the statutory auto-enrolment (AE) route, with adoption highest among smaller firms (77%). Employers appear to be leveraging existing schemes as their primary strategy to meet AE obligations, reflecting strong uptake but also selective compliance approaches.

Implications: Strategic use of existing schemes allows cost control and flexible benefit alignment, but selective compliance may expose organisations to regulatory scrutiny if documentation or gaps arise so due diligence should be shown to ensure fairness and consistency.

The 2026 landscape indicates a more cautious growth trajectory for Irish private sector employers.

Key takeaways include:

Taken together, these trends indicate a shift from post-pandemic expansion to disciplined consolidation. HR leaders must balance cost control, regulatory compliance, and capability development while preparing for demographic, technological, and market challenges.

Join with us in championing better work and working lives across Ireland

Meg is an experienced HR professional, previously working in HRBP roles for Irish public sector and global enterprises. She has a passion for showing the impact of the people profession through creating positive workplace culture. She is qualified to Masters level and is a lifelong learner in the field of people management.

Meg chaired the CIPD Southeast committee in Ireland for 4 years. During that time, she built strong networks providing key learning events and networking opportunities within her region and on the national committee. She began her role as HR Policy and Engagement Manager in August 2022, where she creates value for CIPD customers through the annual calendar of engagement, developing relationships with key stakeholders and wider business community.

Insights, benchmarking data and recommendations from the CIPD's latest survey on employee benefits

Based on an assessment of FTSE 100 annual reports and focus groups with investors and HR leaders, this report gives benchmarking data, insights and practical recommendations for improving workforce reporting practices

The CIPD’s biennial report exploring health, wellbeing and absence management provides invaluable trend analysis and practice insight to help employers and people professionals develop and maintain supportive, productive workplaces

Our research explores how current flexible and hybrid working practices are impacting performance, employee engagement and wellbeing